Highlight 19/2026: The hidden costs of underfunding climate intelligence

Kevin Villacis, 15 June 2026

The policy case for national weather and hydrological services has rested on a simple metric: 1 USD invested in forecasts and early warning systems returns somewhere between 4 USD and 36 USD in avoided losses, according to a recent World Bank systematic review of more than 140 studies. The framing is intuitive and well established: meteorological agencies are technical services, and their value is the disasters they help prevent.

This highlight, drawing on ongoing research at the WMO Development Partnerships Office, argues that the framing understates what these institutions actually do. When a country invests in its meteorological agency, it is not only buying forecasts. It is shaping how the financial markets that lend to the government respond when a climate disaster eventually arrives. The deeper variable is not the size of the budget, but the rule that governs it.

Consider what happens after a major hydrometeorological event in a developing economy. The disaster destroys capital, disrupts supply chains, and reduces tax revenue. The government faces a choice that is rarely framed as a choice at all: should the meteorological agency’s budget shrink alongside the rest of the public sector, or should it be protected? In most climate-vulnerable economies the answer is clear. National Meteorological and Hydrological Services (NMHS) appropriations are tied, formally or informally, to realised GDP. When the economy contracts, so does the weather service.

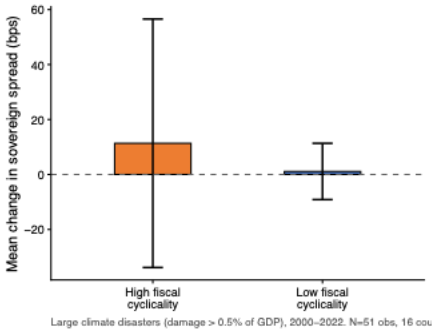

The figure above presents the consequence. Across a panel of 22 climate-vulnerable small open economies, countries with procyclical public spending experience a mean sovereign spread widening of around 11 basis points following large climate disasters. Countries with anchored fiscal rules experience roughly one. The same physical event generates a financial response an order of magnitude larger depending on the institutional environment. International creditors are not pricing the disaster itself. They are pricing what they expect the government to do afterwards.

This is the question that ongoing research at the WMO Development Partnerships Office is examining: why comparable shocks generate such different financial responses across countries. A plausible answer lies in what sovereign creditors can observe. Bondholders cannot directly measure the quality of a country’s hydrological monitoring or forecasting infrastructure, but they can observe how governments behave when revenues contract. A country that protects its meteorological agency through a downturn signal that critical institutional capacity is shielded from short-term fiscal pressure. A country that lets the budget collapse with realised GDP signals the opposite. Over time, those signals are priced, and the meteorological budget becomes a credibility instrument that markets read alongside debt anchors and central bank arrangements.

The analogy with monetary policy clarifies what is at stake. Central bank independence is not defended on the grounds that central bankers are technically superior to finance ministers, but because removing monetary policy from short-term political pressure produces a credibility dividend that lowers the cost of public debt. An anchored meteorological expenditure rule would operate through the same logic: the dividend would flow not through inflation expectations but through climate-risk pricing in sovereign spreads.

The operational template exists in other domains. Chile’s structural balance rule protects fiscal policy from commodity cycles by anchoring expenditure to potential rather than realised revenue. Norway’s Government Pension Fund Global performs the same function for petroleum income. An equivalent arrangement for meteorological appropriations, fixed as a share of cyclically-adjusted GDP, protected by legislative provisions analogous to those governing monetary policy autonomy, would be modest in fiscal cost but consequential in institutional terms.

The tentative conclusion emerging from this work is straightforward. The cost of treating meteorological funding as a discretionary line item is not measured only in forgone forecasts. It is also measured in the basis points a country pays whenever a disaster reveals what its fiscal rule already implied.

Kevin Villacis, Highlight 19/2026: The hidden costs of underfunding climate intelligence, 15 June 2026, available at www.meig.ch

The views expressed in the MEIG Highlights are personal to the authors and neither reflect the positions of the MEIG Programme nor those of the University of Geneva